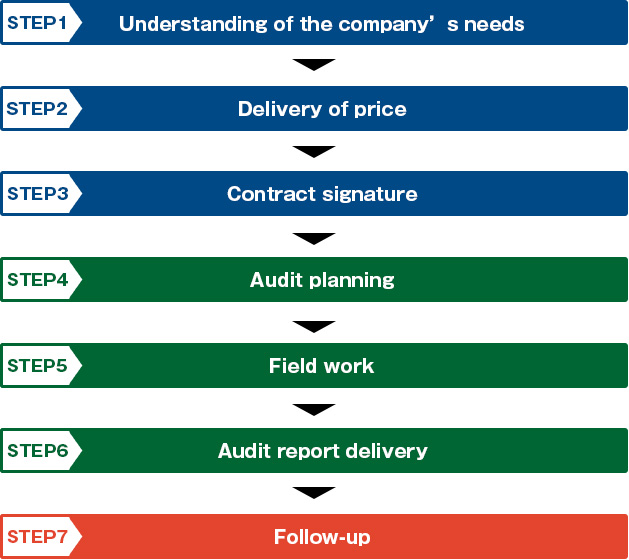

Our team is made by expert auditors from Mexico who are knowledgeable of the local risks as well as Japanese auditors who are familiar with the corporate culture in Japan.

Prokansa auditors are specialized in the corresponding industry, performing high quality work and delivering audit reports in Spanish for local personnel while providing added value with an executive audit report to Japanese Senior-Management. This allows both parties to share and take action based on the audit results and recommendations.

Auditors from Japan Head Office travel from Japan with a frequency of every 3 to 5 years to review general topics, while Prokansa can perform audits on specific areas based on risk analysis, improving frequency and depth.

By being close to the audited, Prokansa is able to follow up and continuously monitor the audit results.

Because local auditors reside in Mexico, Prokansa helps you reduce high costs of traveling from Japan.

It is an independent and objective monitoring and consulting activity designed to add value and improve an organization's operations. Usually, this audit is performed by the internal auditor of the company. It also performs the evaluation of the adequacy of internal controls necessary to achieve the objectives of the company.

It is reviewing the financial statements of a company or any other legal entity based on a set of rules previously established resulting in the publication of an independent opinion on the financial statements. For publicly traded companies, it is mandatory to submit to external audit for the opinion on its financial statements and also the auditors must evaluate internal control of the company to ensure that its financial statements are based on adequate internal control. While for non-listed companies in the stock market this evaluation is not compulsory.

The parent company that holds 100% or majority of the ownership in subsidiaries tends to appoint the Board of Directors silent participants to meet the legal required headcount.The Head Office communicated regularly with the subsidiary and constantly provides instructions and receives reports, this gives the impression that the operations are properly controlled from abroad. Expatriates from Head Office who take the position of Directors many times have been managers of a department; however, do not have the experience in managing an entire company.Subsidiaries typically do not have an internal audit department in their companies and do not have the structure to monitor their continued operation.If there are no relevant problems in the present, subsidiaries tend to believe that there will be no problems in the future: however, when a severe problem occurs, it is too late to take action.Internal Audit is like a medical checkup to prevent further problems is the future.

In the past few years, Japanese companies are aggressively

expanding their operations overseas and especially in Mexico,

which is neighboring the gigantic market of the United States and

has Free Trade Agreements with 47 countries of the world,

promoting free commerce, for example, the Japanese Automotive

factories come together in the Bajio region to build new plants, as

well as other auto part manufacturers and service companies

related to this great investment in the automobile industry.

For subsidiary companies to be able to achieve their goals in a

timely manner there is a need to be more independent in the

decision making process, and be empowered to act upon those

decisions. However, this represents an increase in risk as the

subsidiary will have the ability to generate loss and affect the

Corporations’ bottom line or damage the image of the Corporation

proportional to the power given to the subsidiary company. To

promote the growth of the Corporation in a healthy management

environment, it becomes more and more important for the Head

Office to be able to monitor the subsidiary through a strong

Corporate Governance model and for the subsidiary to have a good

risk management culture.

5

Under such circumstances, Senior Management increasingly

demands the Head Office Internal Audit department to perform

audits to the subsidiaries located abroad using its limited resources

in budget and personnel. The Japanese companies have started to

outsource areas such as Human Resources, Payroll, Information

Technology, which are areas identified as non-core within the

company. Global companies in Europe and North America are

already starting to outsource Internal Audits in order to achieve a

better cost benefit.

Prokansa intends to provide the solution to those needs for

companies which are looking for Internal Audit outsourcing.

| Company name | Prokansa LLC. |

|---|---|

| Establishment date | June 12th,2015 |

| Major activity | Risk management consulting |

| Offices in Mexico | Serafin Olarte no.26-2,Colonia Independencia,Mexico,D.F. Camino de los Cerezos 417, Lomas de Gran Jardín León Gto. |

| Office in Japan | Hikarigaoka 3-7-11-103, Nerima-ku, Tokyo |

| E-MAIL adress | shinichi.hara@prokansa.com |

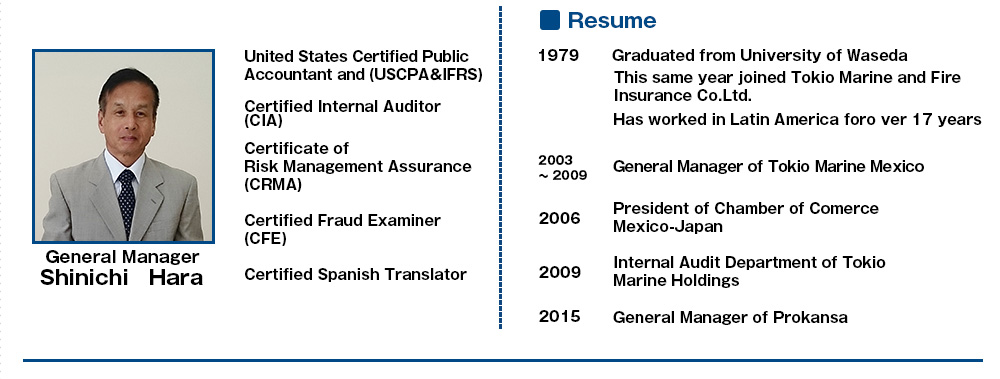

In 1973, during my junior year of High School, I had the opportunity to obtain a scholarship to go to Costa Rica from Central America. This was my first contact with Latin America. Since then, I have been within the Latin American environment. In the last 40 years I have experienced the light and the shadow of Latin America, and I have been a witness to the Japanese companies and its day to day challenges in an environment completely different from Japan. In my previous work, I was an employee of an insurance company and my main task was to suggest solutions to the risks that surrounded the companies. I was responsible for a subsidiary of a Japanese Company and I experienced making decisions and taking actions upon risks which could not be covered by insurance. Taking advantage of this experience, it is a joy for me to be able to help in the achievement of Japanese companies’ goals in Latin America, especially in Mexico, through Risk Management.

Copyright PROKANSA. All Rights Reserved.